The Real Cost of Contact Center Authentication: Part 2 – Security Costs

January 5, 2024 | Contact Center Optimization

In the previous post, we explored the operating costs associated with authenticating callers in the contact center. In addition to the drain on time for agents to go through (on average), a minute and a half of Q&A, there are also additional costs related to account security. Here are troubling statistics around the vulnerability of the call center and how easy it is for fraudsters to get what they need to break into member or customer accounts.

- 2021 saw a 79% increase in losses from identity fraud (Javelin Strategy & Research)

- 37.2 Billion personal records were exposed in data breaches in 2020 (Security Magazine)

- An individual’s complete digital profile with financial info on the “Dark Web” only costs $4 (Flashpoint)

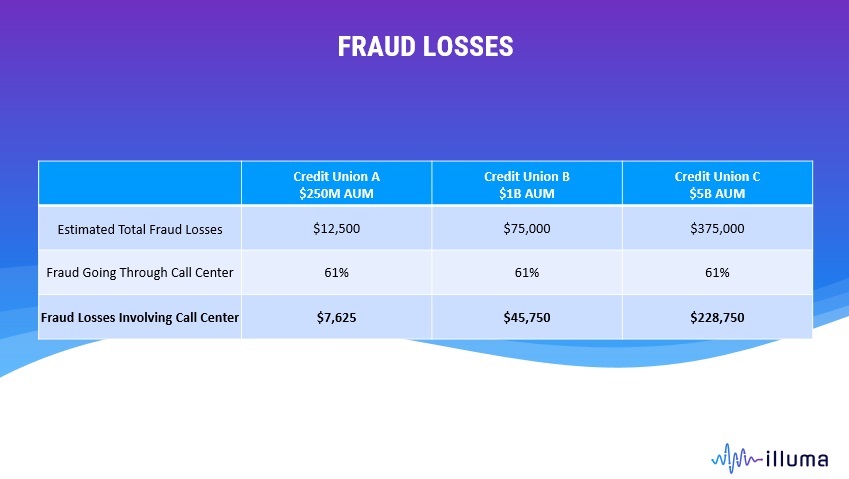

- 61% of fraud losses from account takeovers involve the call center (Aite Group)

What does this mean in dollars and cents for a credit union or community bank? Even a small financial institution is likely to lose thousands of dollars through contact center fraud. A large institution could be looking at hundreds of thousands. The damage to brand reputation and customer/member trust adds to this burden and recovery can be difficult.

Security Q&A Gets a Failing Grade

Let’s explore the costs associated with security that simply doesn’t work well. Out of wallet questions are particularly prone to both false negatives and false positives. Real account holders often forget the correct answers to their security questions and get locked out of their accounts. At the same time, well-prepared fraudsters can defeat security Q&A with relative ease using stolen personal information.

The data around authentication is concerning. Gartner researchers have found that about 30% of legitimate callers trigger a false negative during the identity verification process while well prepared fraudsters can trigger a false positive as much as 60% of the time.

Refusing access to legitimate callers while allowing fraudsters in is a nightmare scenario for credit unions and community banks. The frustration of members and customers who can’t access their accounts represents another hidden cost for security. Reputation cost can be hard to quantify, but it has a very real impact as well.

What about Step Up Authentication?

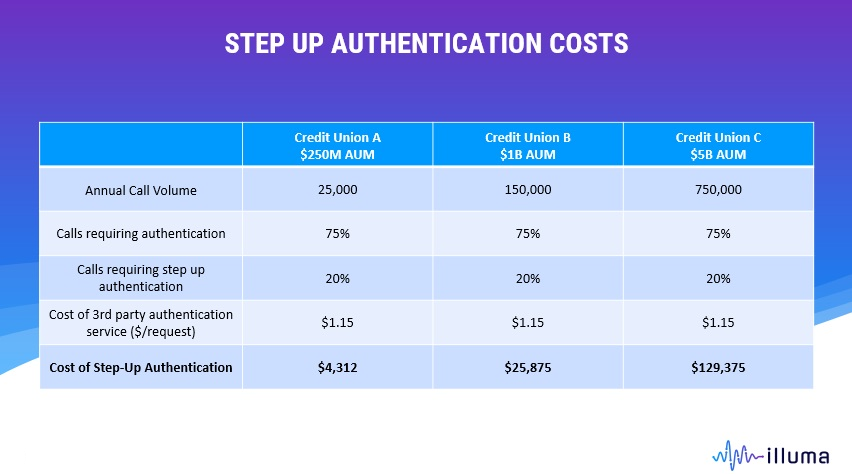

Often banking call centers realize that the out-of-wallet questions are insufficient. Step up authentication may be instigated for suspicious calls or high-risk transactions. Typical 3rd party authentication services can cost more than a dollar per call. Assuming 3 out of 4 calls require authentication, even if only 20% of these interactions include step-up authentication, the cost can be significant.

Between fraud losses and 3rd party authentication, credit unions are spending five to six figures per year on caller verification above and beyond operating costs that can run as high as half a million a year for a large credit union. Next, we’ll explore another authentication expense that is often overlooked – the time and opportunity cost to members and customers.

1.Litan, Avivah. Absolute Identity Proofing Is Dead; Use Dynamic Identity Assessment Instead. Gartner, Inc., 16 Nov. 2015